How credit-worthy are you?

And why it matters

Most people probably had that one friend in college who was always borrowing money - most of the time they paid you back, sometimes they didn’t. And some people were probably fine with it, while others were reluctant to lend to this person again.

That worked out fine when you were in college; you were dealing with relatively small amounts, and it would not have significantly impacted your spending ability. But once you start earning and your spending power increases, when you do need to borrow funds, you are likely to borrow much larger amounts.

Subsequently, the entity/person you borrow from (known as the creditor) is very unlikely to be someone you know personally. It is also highly unlikely that the lender of these funds will be as casual as your college friends about your ability to pay it back.

That brings in a problem - how is a complete stranger, the creditor, going to judge the likelihood of you repaying the borrowed funds? To solve this problem, the credit score was created.

But what is a credit score?

In simple terms, an individual’s credit score is a measure of how likely they are to be able to repay borrowed funds. As is the case with most things in a society with a practically infinite number of people, we try to boil down this likelihood into a single number. This number is known as a credit score and typically ranges from 300 to 900. The higher your score, the more credit-worthy you are considered.

Your credit score is calculated on the basis of your credit history, including key factors like:

Payment History: This is the record of whether you've paid your credit accounts on time and is the single most important factor in determining your credit score. Late payments can have a negative impact on your score.

Credit Utilization: This is the ratio of your current credit card balances to your credit limits. High credit card balances relative to your credit limits can negatively affect your score.

Length of Credit History: The amount of time you've had credit accounts can impact your score. A longer credit history is generally viewed more favorably.

Types of Credit in Use: This considers the variety of credit accounts you have, such as credit cards, mortgages, and installment loans.

New Credit: Opening several new credit accounts in a short period can negatively impact your score.

There are 4 RBI-regulated bodies, CIBIL, Experian, CRIF High Mark and Equifax, that offer official credit scores on the basis of these and other factors they consider relevant. They each have their own method of calculating credit scores.

If you have never utilized credit in any form, your credit score will not exist. When you don’t have a credit score, lenders estimate your credit-worthiness on the basis of factors such as your annual income, profession, and other financial information. But maybe you’re young, and don’t foresee the need for any kind of credit in the near future. Even in such a situation, building a solid credit score can prove beneficial.

Why should you care about your Credit Score?

Your credit score is essentially a measure of how financially sound the system considers you to be. And unless you plan to live off the land, it is highly likely that you will avail credit at some point in your life, be it in the form of a personal loan, mortgage or even just a credit card.

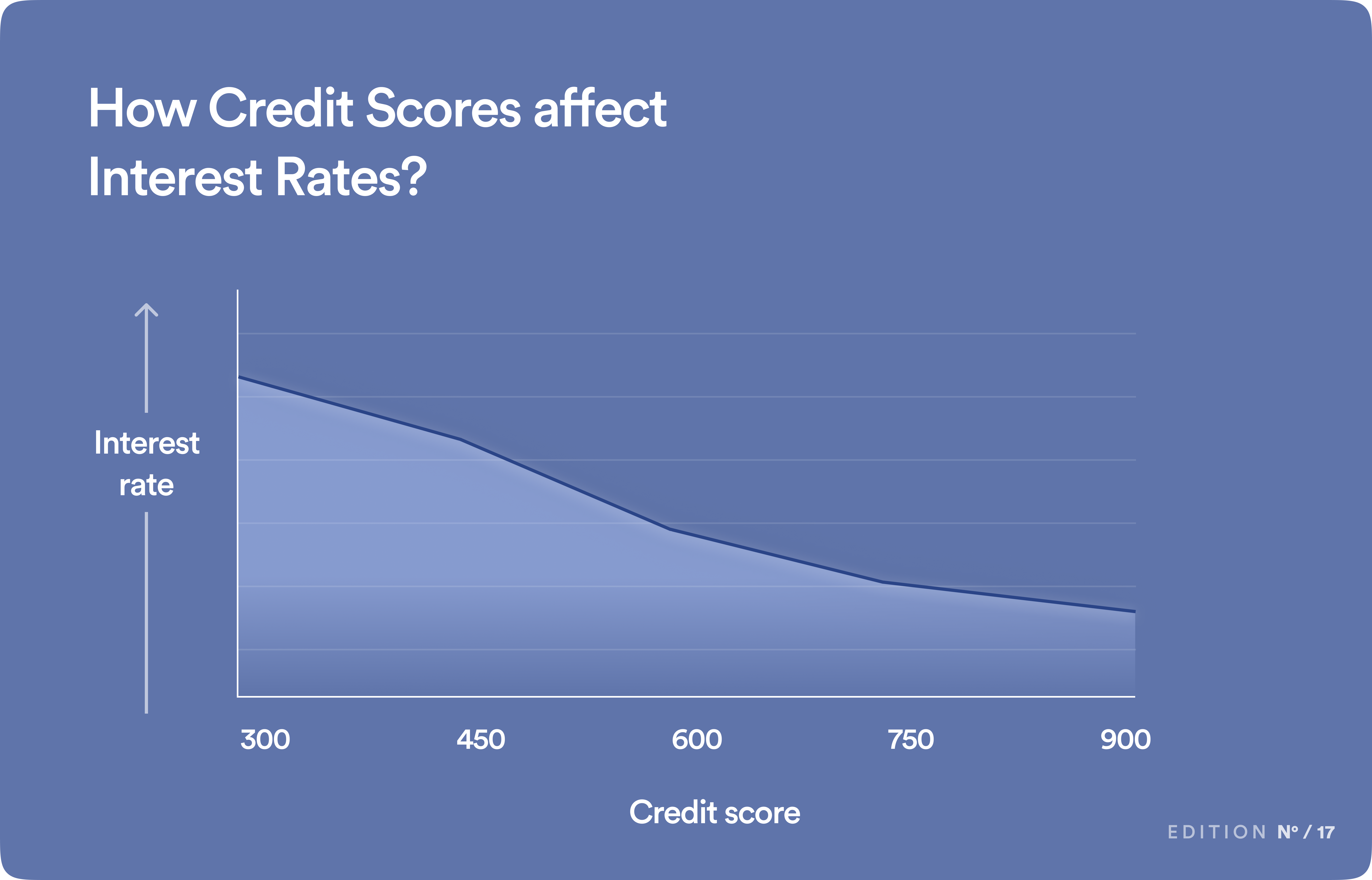

Having a good credit score comes with its own benefits. For example, loan approvals are highly dependent on your credit score, and having a high credit score often leads to lower interest rates on loans. Your credit score also dictates your eligibility for better credit cards and even affects your credit limit.

As an essential component of the global economy, tapping into credit can greatly expand your financial capabilities, so improving your access to cheap credit is always a good idea.

But what if I have a poor credit score?

Don’t worry, while having a good credit score is definitely beneficial, all is not lost if you have a poor credit score. Credit can still be availed in the form of products such as loans against mutual funds, loans against FDs, or essentially any credit with some form of collateral to offset the creditor’s losses in case of default.

The downside is that your credit is limited to the value of the assets you are willing to put up as collateral. But by repaying expensive loans through usage of such products, you can slowly rebuild your credit score and improve your access to credit.

Establishing your credibility in the eyes of the financial system takes time, and taking on small amounts of credit and reliably repaying it is a good way to start.

Refer your friends to help them start building a stable financial portfolio and ensure they can access credit when they need it.

In today’s edition, we’ve shown you what a credit score is and why it is important to maintain it at a stable level. At Stable Money, we’re going to keep you informed and ensure that you make the best financial decisions.

Best, Team Stable Money

How do I know the interest rates for a home loan that I can fetch based on my credit score? and how do these rates vary with the credit score?